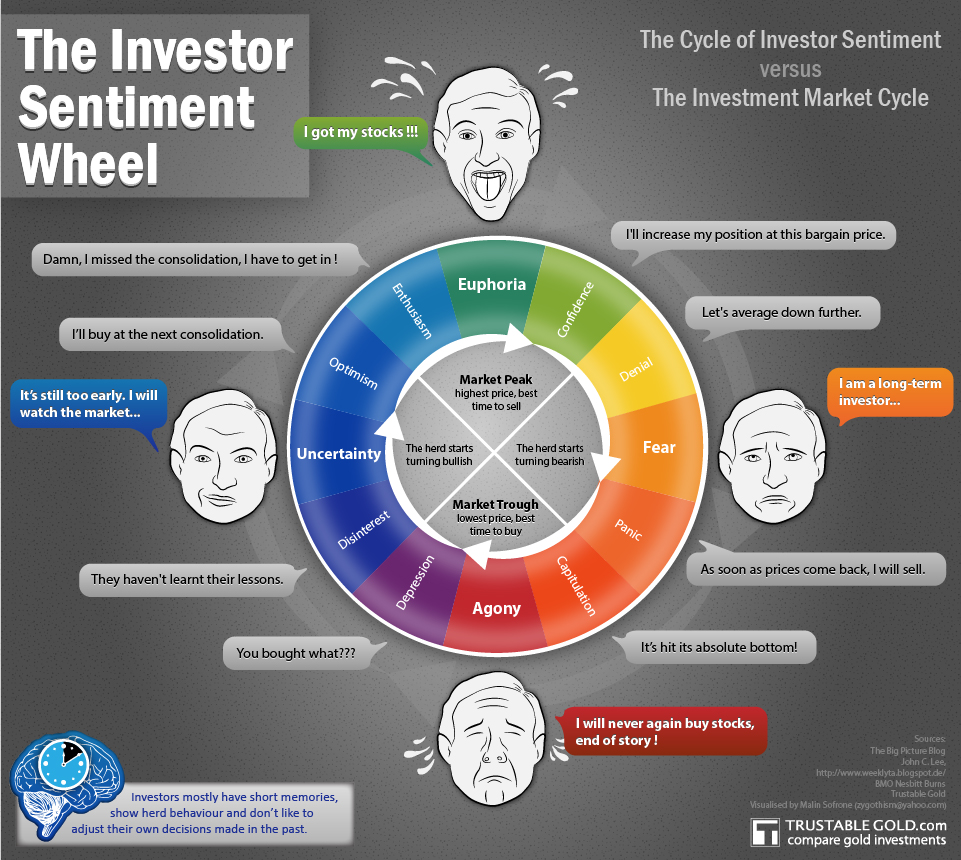

And it has this kickass image as well. Make sure you enlarge and enjoy!

My interpretation of the Libor scandal is the obvious one: banks, as presently constituted and managed, cannot be trusted to perform any publicly important function, against the perceived interests of their staff. Today’s banks represent the incarnation of profit-seeking behaviour taken to its logical limits, in which the only question asked by senior staff is not what is their duty or their responsibility, but what can they get away with.

September 26, 2007: The Financial Times – Gillian Tett: Libor’s value is called into questionOne of these is a growing divergence in the rates that different banks have been quoting to borrow and lend money between themselves. For although the banks used to move in a pack, quoting rates that were almost identical, this pattern broke down a couple of months ago – and by the middle of this month the gap between these quotes had sometimes risen to almost 10 basis points for three month sterling funds. Moreover, this pattern is not confined to the dollar market alone: in the yen, euro and sterling markets a similar dispersion has emerged. However, the second, more pernicious trend is that as banks have hoarded liquidity this summer, some have been refusing to conduct trades at all at the official, “posted” rates, even when these rates have been displayed on Reuters.April 16, 2008: The Wall Street Journal – Bankers Cast Doubt On Key Rate Amid Crisis

The concern: Some banks don’t want to report the high rates they’re paying for short-term loans because they don’t want to tip off the market that they’re desperate for cash. The Libor system depends on banks to tell the truth about their borrowing rates. Fibbing by banks could mean that millions of borrowers around the world are paying artificially low rates on their loans. That’s good for borrowers, but could be very bad for the banks and other financial institutions that lend to them.May 2, 2008: The Wall Street Journal – Libor’s Guardian Bristles At Bid for Alternative Rate

The group that oversees a widely used interest rate fired back Thursday at an effort to introduce an alternative to the rate, known as the London interbank offered rate, or Libor. In recent weeks, the British Bankers’ Association, which calculates Libor, has faced questions about the accuracy of the rates that a 16-bank panel submits to reflect their dollar-denominated borrowing costs. The group said a review of how Libor is calculated “is due to report shortly,” though it declined to offer an exact date. It also noted that any substitute for Libor — which is supposed to reflect the rates at which banks make short-term loans to one another — would have to meet high standards to “win the market’s confidence.” On Wednesday, ICAP PLC, a London broker-dealer with offices in New York, said it plans to launch a new measure of the rates at which banks borrow dollars. ICAP expects to begin publishing the rate, known as the New York Funding Rate, or NYFR, as soon as next week, said Lou Crandall, chief economist at Wrightson ICAP, a New Jersey research firm that is part of the ICAP group. Mr. Crandall said NYFR isn’t intended to replace Libor.September 24, 2008: The Wall Street Journal: Libor’s Accuracy Becomes Issue Again

Questions on Reliability of Interest Rate Rise Amid Central Banks’ Liquidity Push

Earlier this year, Libor appeared to be sending false signals. Banks complained to the BBA that rival banks might not be reporting their true borrowing costs because they didn’t want to admit that others were treating them as if they had troubles. That led to a BBA review and the pledge that the rates banks contribute would be better policed. Every morning, 16 banks submit borrowing rates in a process that produces Libor rates at lunchtime in London.October 20, 2008: The Wall Street Journal – Bank-Lending Boost Could Spur Thaw

On Friday, three big banks led by J.P. Morgan Chase & Co. made multibillion-dollar offers of three-month funds to European counterparts, causing an immediate stir in the shriveled markets for unsecured lending. That raised expectations that lenders would finally open their doors and businesses would be able to borrow again, removing one of the biggest stresses on the global economy.In the story above (October 20, 2008), JP Morgan, a two trillion dollar bank, made $10 to $15 billion of LIBOR loans to other multi-trillion dollar banks and then proudly announced that LIBOR rates had fallen, the market was thawing and the credit crisis was easing. As we wrote in 2008, this was nothing short of rigging the market.Sum it up and all the revelations we are reading about this week were already evident about four years ago. None of should be surprising. As Jean-Claude Juncker told us last year, “when it becomes serious, you have to lie.”

My initial diagnosis is this: whether formally or informally, you have two groups of banks submitting rates for LIBOR. One group is trying to pull LIBOR up, the other is trying to pull LIBOR down. Statistically, if I add up their intercept terms from the first table, they both sum to 0.23%, one positive, the other negative. Even if LIBOR were a simple average, which it is not, this is a colossal game of tug of war, with two equal teams.As it is, LIBOR excludes the outliers, and calculates an average off of those that remain. It’s a difficult measure to manipulate. There may have been attempts to manipulate LIBOR, and even two groups of banks trying to pull LIBOR their own way, but successful systemic manipulation of LIBOR is unlikely in my opinion.But if you disagree, here are the two clusters of banks, pursue their collusions:Coalition to pull LIBOR up

- Barclays

- BTMU

- Credit Suisse

- HBOS

- Norinchuckin

- RBS

Coalition to pull LIBOR down

- Citi

- HSBC

- JP Morgan

- Lloyds

- Rabobank

Start with Barclays and JP Morgan, they are the outliers, and if there is collusion, they are the likely leaders.

In connection with the Merger described in Item 2.01 of this Current Report on Form 8-K and pursuant to the terms of the Merger Agreement, effective as of the effective time of the Merger, William D. Johnson, the former Chairman, President and Chief Executive Officer of Progress Energy, was appointed as the President and Chief Executive Officer of Duke Energy.Mr. Johnson, age 58, was Chairman, President and Chief Executive Officer of Progress Energy, from October 2007 through July 2, 2012. … Mr. Johnson previously served as President and Chief Operating Officer of Progress Energy, from January 2005 to October 2007.Mr. Johnson subsequently resigned as the President and Chief Executive Officer of Duke Energy. See disclosure below under the heading “Resignation of Mr. Johnson and Reappointment of Mr. Rogers.”

For his part, Mr. Johnson has received a lucrative exit package, according to a securities filing. He will receive payments of about $44 million, which includes a $7.4 million severance. He receives a lump-sum payment of $1.5 million so long as he does not disparage Duke and cooperates with the company.

3 July 2012Barclays PLC and Barclays Bank PLC (Barclays)Board changesBarclays today announces the resignation of Bob Diamond as Chief Executive and a Director of Barclays with immediate effect. Marcus Agius will become full-time Chairman and will lead the search for a new Chief Executive. Marcus will chair the Barclays Executive Committee pending the appointment of a new Chief Executive and he will be supported in discharging these responsibilities by Sir Michael Rake, Deputy Chairman.The search for a new Chief Executive will commence immediately and will consider both internal and external candidates. The businesses will continue to be managed by the existing leadership teams.Bob Diamond said “I joined Barclays 16 years ago because I saw an opportunity to build a world class investment banking business. Since then, I have had the privilege of working with some of the most talented, client-focused and diligent people that I have ever come across. We built world class businesses together and added our own distinctive chapter to the long and proud history of Barclays. My motivation has always been to do what I believed to be in the best interests of Barclays. No decision over that period was as hard as the one that I make now to stand down as Chief Executive. The external pressure placed on Barclays has reached a level that risks damaging the franchise – I cannot let that happen.I am deeply disappointed that the impression created by the events announced last week about what Barclays and its people stand for could not be further from the truth. I know that each and every one of the people at Barclays works hard every day to serve our customers and clients. That is how we support economic growth and the communities in which we live and work. I look forward to fulfilling my obligation to contribute to the Treasury Committee’s enquiries related to the settlements that Barclays announced last week without my leadership in question.I leave behind an extraordinarily talented management team that I know is well placed to help the business emerge from this difficult period as one of the leaders in the global banking industry.”Commenting, Marcus Agius said, “Bob Diamond has made an enormous contribution to Barclays over the last 16 years of distinguished service to the Group, building Barclays Investment Bank into one of the leading global investment banks in the world. As Chief Executive he has led the bank superbly. I look forward to working closely with the Chief Executives of our businesses and the other members of the executive Committee in leading Barclays world class businesses in serving our customers and clients and delivering value for our shareholders.”